How Proactive Longevity Care Is Planned and Paid For

FLOW pays for plannable services and products with an individually owned spending account.

Longevity and healthspan are not accidental outcomes—they are the result of deliberate, forward-looking decisions and actions taken over decades. Yet traditional healthcare finance treats most health spending as reactive, episodic, and claim-driven, forcing even proactive care into systems designed for acute intervention. FLOW starts from a different premise: if health outcomes are planned, the funding behind them must be planned as well.

At the center of this approach is person-centered planning. Rather than allowing insurance coverage rules or provider incentives to dictate care, individuals define their own health and longevity priorities—training, prevention, recovery, optimization, and routine medical needs—based on their goals, risks, and life stage. These decisions do not belong in a claims-based system designed to manage uncertainty.

FLOW funds these proactive decisions through a fully individual-owned health spending account. This account is not insurance, not a benefit allowance, and not a reimbursement vehicle. It is a direct funding mechanism for planned health and longevity investments, owned entirely by the individual and used intentionally for care that is expected, chosen, and aligned with long-term health goals.

Because spending is planned and owned, claims friction disappears. There are no utilization thresholds to trigger, no coding games to play, and no incentives to delay care until it becomes medically necessary. Preventive services, training programs, diagnostics, and routine care can be funded when they are most effective—not when they become unavoidable.

This distinction matters. When proactive health decisions are forced through insurance, they are either discouraged, underutilized, or distorted by coverage rules designed for rare and expensive events. By separating planned care from insurance entirely, FLOW removes the structural penalty for investing early and consistently in healthspan.

This distinction reflects the broader role of longevity care[/longevity-care]—a system designed to manage healthspan intentionally, alongside but separate from healthcare. In practical terms, this means individuals experience clarity and control: what is planned is funded directly, transparently, and without adversarial incentives. Health decisions become investments rather than claims, and longevity becomes something that is actively built—not passively hoped for.

Covering Unplanned Health Events Without Distorting Everyday Decisions

FLOW uses a sponsored risk assurance pool to fund predictable, but unplannable, healthcare finance needs.

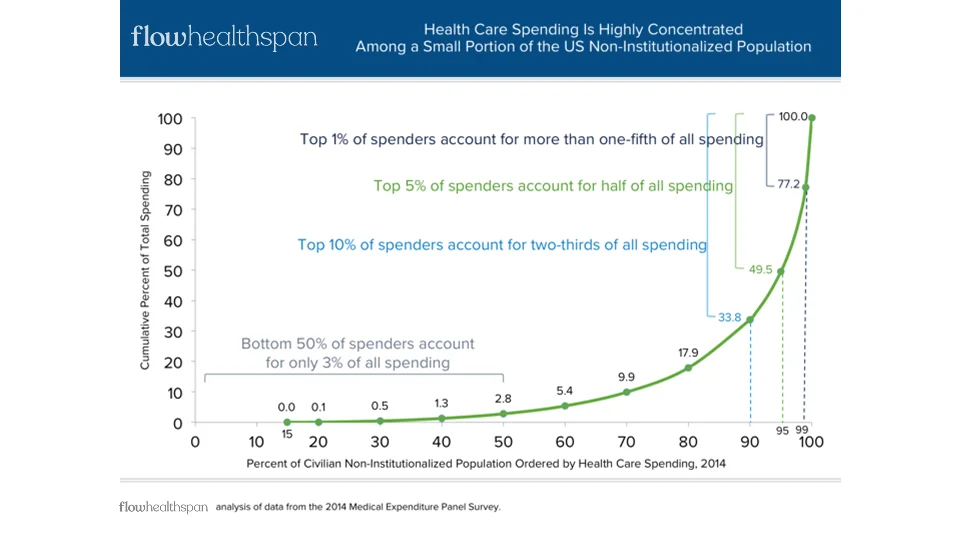

Not all health events can be planned—but not all unplanned events are catastrophic either. Between predictable, proactive care and truly life-altering medical crises lies a broad middle ground: injuries, acute illnesses, unexpected procedures, and short-term disruptions that are financially meaningful but not system-breaking. Traditional insurance collapses this entire middle layer into the same claims-driven machinery used for catastrophic risk, with predictable consequences.

FLOW addresses this gap through a sponsored community assurance pool. Rather than treating every unplanned event as an insurance claim, the assurance pool spreads mid-level health risk across a defined community, allowing individuals to recover from unexpected events without distorting everyday health decisions or introducing adversarial incentives.

This distinction matters because unplanned does not mean unpredictable at the population level. While no individual can know when they will break a bone or need an urgent procedure, the frequency and cost distribution of these events across a community are remarkably stable. That makes them well-suited for structured risk sharing—without the overhead, exclusions, and incentive misalignment of insurance.

This middle layer is especially critical for grey-zone individuals [/grey-zone-health-coverage]— those with ongoing but manageable risk that does not justify full insurance treatment.

The assurance pool is intentionally bounded. It covers defined categories of mid-level health events up to a clear upper limit, ensuring that it protects individuals from meaningful financial disruption while avoiding open-ended exposure. By design, it does not absorb routine care or preventive services, and it does not replace catastrophic insurance. Its role is precise: to absorb manageable uncertainty while preserving the integrity of proactive health planning.

Because the pool is sponsored—often by employers—it aligns incentives in a fundamentally different way. Sponsors benefit when communities are healthier, recover faster, and avoid escalation into catastrophic care. Individuals benefit from coverage that activates when needed without penalizing proactive behavior or encouraging overutilization.

The result is a layer of protection that feels supportive rather than adversarial. Unplanned health events are addressed quickly and predictably, while everyday health decisions remain grounded in planning, ownership, and long-term goals—not claims eligibility or cost-shifting.

Why Catastrophic Health Insurance Is Reserved for Financially Ruinous Risk

FLOW uses catastrophic health insurance where it is best suited- transferring risk of low probability, high-impact events.

Insurance plays an essential role in any functional health system—but only when it is used for the problem it is designed to solve. Catastrophic health insurance exists to protect individuals and families from low-probability, high-severity medical events that would otherwise be financially ruinous. When insurance is asked to fund routine or mid-level care, it becomes expensive, adversarial, and misaligned by design.

This restraint matters because insurance-driven price formation [https://chatgpt.com/cash-self-pay-vs-insurance-rates] routinely inflates the cost of care when applied outside true catastrophic risk.

FLOW deliberately confines insurance to a narrow but critical role: low-probability, high-impact events. True catastrophic events—major trauma, complex cancer care, organ failure, prolonged hospitalization, or other life-altering medical crises—are not meaningfully plannable at the individual level. Their costs are large, their timing is unpredictable, and their financial impact can overwhelm even disciplined savers. These are precisely the conditions under which insurance is both necessary and appropriate.

In the FLOW model, catastrophic health insurance is activated only after the upper limit of the community assurance pool is reached. This boundary is intentional. The assurance pool absorbs manageable uncertainty and mid-level costs, while insurance is reserved for tail-risk events that exceed defined thresholds. The handoff between these layers is explicit, not ambiguous, preventing cost-shifting and coverage creep.

This structure protects all participants. Individuals are shielded from financially ruinous outcomes without being forced to route everyday health decisions through claims systems. Sponsors benefit from bounded exposure rather than open-ended liability. Insurers are returned to their proper function: risk management for rare, severe events—not administrators of routine care.

By restoring insurance to its intended purpose, FLOW removes it from places where it distorts behavior and preserves it where it matters most. The result is a cleaner system with clearer boundaries, fewer conflicts, and a funding structure that treats catastrophic risk with the seriousness—and restraint—it requires.

A Unified Model for Health Costs Across Risk and Time Horizons

Most healthcare finance systems treat all health and longevity spending as a singular problem. It isn’t.

Health spending spans multiple dimensions: planned versus unplanned, small costs versus large costs, short-term needs versus long-term outcomes. When these fundamentally different categories are forced through a single financial mechanism, inefficiency and misaligned incentives are inevitable. FLOW’s funding model works because it does the opposite—it matches each type of health decision to the financial tool best suited to it.

Planned, proactive health investments sit at one end of the healthcare and longevity care financial spectrum.

These decisions—training, prevention, diagnostics, optimization, and routine services—are predictable, intentional, and repeated over time. They benefit from clarity, ownership, and direct funding, not risk pooling or claims adjudication. This is why they are funded through individual-owned spending accounts designed explicitly for planning and control.

At the other end of the spectrum are catastrophic medical events handled through true insurance and risk transference.

These are rare, severe, and financially ruinous. They require large-scale risk transfer and are appropriately handled through insurance—activated only when defined thresholds are exceeded and other funding layers are exhausted.

Between these poles lies the broad middle ground of unplanned but manageable health events.

These events are unpredictable at the individual level but stable at the population level, making them ideal candidates for structured risk sharing. Sponsored community assurance pools occupy this middle layer, absorbing uncertainty without distorting everyday health and longevity decisions or expanding insurance beyond its intended role.

Viewed together, these three layers form a comprehensive strategic system rather than a patchwork. Costs are addressed according to their predictability and impact, incentives are aligned across time horizons, and no single mechanism is forced to do work it was never designed to do. The result is lower total system cost—not through denial or delay, but through better matching of risk, responsibility, and funding.

This is the core insight behind the FLOW model: when health decisions are funded in proportion to their nature and risk, individuals gain control, sponsors gain predictability, and insurance regains its legitimacy. Health spending becomes intelligible, intentional, and sustainable across a lifetime.

What the FLOW Healthcare Finance Model Means in Practice

FLOW’s funding model is not just a structural redesign of healthcare finance—it changes how responsibility, risk, and decision-making are experienced by the people inside the system. By separating planned care, shared risk, and catastrophic protection into distinct but connected layers, FLOW clarifies who pays for what, when, and why. That clarity has different—but complementary—implications for employers and individuals.

This structure operationalizes person-centered care planning [/person-centered-care-healthcare-finance] by aligning authority, planning, and funding with the individual rather than institutional incentives.

What It Means for Employers

From insurance buyers to sponsors of sustainable health assurance

For employers, FLOW represents a shift away from being passive purchasers of increasingly expensive insurance products and toward becoming active sponsors of employee health and longevity assurance. Rather than underwriting open-ended utilization through premiums, employers sponsor a clearly defined assurance layer that addresses mid-level, unplanned health events within explicit boundaries.

This sponsorship model creates predictability. Financial exposure is bounded, costs can be modeled, and investments in employee health are no longer disconnected from outcomes. Because proactive and routine care are funded separately through individual-owned accounts, employer-sponsored assurance is not burdened by everyday utilization or distorted by coverage design.

The incentives also change. Employers benefit when employees invest early in healthcare and longevity care, recover quickly from setbacks, and avoid escalation into catastrophic care. Sponsored assurance aligns employer economics with employee well-being, reducing the adversarial dynamics that often emerge in claims-driven systems.

Most importantly, FLOW allows employers to reframe healthcare and longevity care spending as a strategic investment rather than an uncontrollable cost. Health becomes something that can be planned, supported, and measured over time—without requiring employers to manage care or assume insurer-like roles.

What It Means for Individuals

Ownership, clarity, and health decisions that actually compound

For individuals, FLOW restores ownership and true agency—qualities largely absent from traditional healthcare finance. Planned health and longevity decisions are funded through accounts they fully own and control, allowing them to invest in prevention, training, diagnostics, and routine care without navigating claims, coverage rules, or utilization penalties.

Unplanned health events are addressed through community assurance in a way that feels supportive rather than adversarial. Coverage activates when needed, without forcing individuals to delay care or reshape decisions to fit insurance requirements. Clear boundaries between assurance and insurance remove uncertainty about what happens when costs escalate.

This clarity changes behavior. Health decisions no longer feel like gambles against deductibles or coverage limits. Instead, individuals operate with a simple mental model: what I plan, I fund; what we share, the community supports; what is truly catastrophic, insurance protects.

Over time, this structure encourages consistency, reduces fear-driven decision-making, and allows health and longevity investments to compound. Longevity becomes an active pursuit, supported by a financial system designed to reinforce—not undermine—long-term health goals.

Closing Perspective: Why Separating Health Decisions from Insurance Incentives Matters

Healthcare finance fails not because people make poor health decisions, but because the system asks the wrong financial tools to do the wrong jobs. Insurance is used where planning would be more effective, planning is constrained by coverage rules, and individuals are left navigating incentives that reward delay, escalation, and fragmentation.

FLOW starts by separating health decisions from insurance incentives—then rebuilding the funding model around that separation. Planned health and longevity investments are funded directly and owned by the individual. Unplanned but manageable risks are shared at the community level. True catastrophic risk is insured, and only insured. Each layer does the work it is suited to do, without spilling into the others.

This separation restores coherence. Health decisions become intentional rather than reactive. Risk is shared without distorting behavior. Insurance regains legitimacy by focusing on financially ruinous events rather than routine care. Costs fall not through denial or rationing, but through alignment—matching responsibility, risk, and funding across time horizons.

Executing this model over time requires coordinated guidance [/why-longevity-care-requires-teams]—not isolated expertise—across financial, clinical, and longevity domains.

Most importantly, this model reframes healthcare finance around human health rather than institutional process. It gives individuals control without isolating them, gives employers predictability without forcing them into insurer roles, and gives the system a path toward sustainability without sacrificing outcomes.

When health decisions are planned like investments and protected like risks, longevity care stops being an abstract ideal and becomes something that can be built—deliberately, transparently, and over a lifetime.