The Grey Zone — Where Today’s Healthcare Model Begins Breaks Down

Not Fully Healthy, Not Actively Ill

At a population level, most people do not move discretely from health to illness. Instead, they pass through a long, gradual middle ground—one where they remain functional, engaged, and capable, but where health becomes more variable, care more complex, and costs less predictable. This is the grey zone. For some, it appears earlier due to genetics, injury, or chronic conditions. For everyone else, it arrives later through aging alone.

Over time, recovery slows, baseline risk rises, and small issues carry greater consequence. Care shifts from being occasional and incidental to ongoing and coordination-heavy. Even without a single defining diagnosis, individuals find themselves managing medications, monitoring labs, navigating specialists, and making more deliberate tradeoffs about prevention, lifestyle, and care. They are not “sick” in the traditional sense—but their healthcare is no longer cheap, simple, or well served by systems designed for episodic intervention.

Autoimmune, metabolic, genetic, neuro-inflammatory, chronic pain, and mental health conditions are common early examples of this pattern, but the pattern itself is universal. Age is the unifying factor. It steadily increases healthcare cost, complexity, and variability, pushing everyone—eventually—out of the category of effortless health and into the grey zone. This phase requires longevity care[/longevity-care]—a system designed to manage healthspan over time rather than respond episodically to breakdown.

The challenge is not that people enter this phase. The challenge is that our healthcare and healthcare finance models are not designed for it and do a poor job of managing the risks it presents.

Why This Population Is Structurally Misfit by Insurance

Traditional health insurance is built around an episodic intervention model. People are either broadly healthy and inexpensive—requiring little attention—or they are ill, expensive, and expected to be resolved through acute intervention. Coverage, utilization controls, and care pathways reflect this assumption: an event occurs, resources are deployed, and once the episode concludes, the system disengages until the next failure.

This model works reasonably well for discrete events like infections, injuries, or surgeries. It breaks down for people whose health does not follow an episodic pattern. Grey-zone individuals are not “broken” in a way that can be fixed and forgotten. Their needs are ongoing, longitudinal, and coordination-heavy—requiring sustained attention rather than episodic response.

Because insurance is not designed to support continuity, optimization, or long-term planning, these individuals are not supported—they are managed. Their care is shaped by utilization controls, denials, and administrative friction intended to mitigate cost, shifting the burden of coordination and persistence onto the individual. Preventive and stabilizing interventions are undervalued, financial access is restricted rather than planned, and meaningful support often arrives only after deterioration occurs.

The Hidden Cost of Living in the Grey Zone

The burden of the grey zone isn’t just financial. It’s cognitive and emotional. People spend years navigating uncertainty—wondering what’s covered, what isn’t, which provider to trust, and how to plan for a future that feels statistically riskier but medically stable. Small decisions carry outsized weight. A missed lab, delayed follow-up, or poorly coordinated change in care can cascade into avoidable escalation. Much of this burden is amplified by insurance-driven price formation[/cash-self-pay-vs-insurance-rates], where routine services are priced for claims processing rather than direct, coordinated care.

This constant background uncertainty creates stress that traditional models rarely account for. Even well-resourced individuals can feel exposed, while employers and payors struggle to distinguish unavoidable cost from preventable deterioration. The system reacts after problems surface, rather than supporting the planning and coordination that could keep them from arising in the first place.

The grey zone isn’t a niche edge case—it’s a structural blind spot. And understanding it clearly is the first step toward fixing how health coverage, care planning, and risk are handled across a lifetime.

Longevity Care When Risk Is Non-Zero

Why Proactive Care Matters More When Risk Exists

When health risk is elevated, the value of proactive care increases. Grey-zone individuals don’t need dramatic rescue interventions; they need stability, foresight, and early course correction. Small deviations in sleep, stress, inflammation, medication adherence, or lifestyle can compound over time, quietly increasing the likelihood of escalation. Addressing those signals early is both clinically smarter and economically sound.

Systems optimized for acute response struggle here. Longevity care, by contrast, is built around continuity: monitoring trends, optimizing behaviors, adjusting plans, and intervening before instability becomes failure. For people whose health is variable but manageable, this difference matters enormously.

Augment Health Insurance — It Doesn’t Replace It

FLOW, as an inherently proactive longevity care platform, does not attempt to replace health insurance, nor does it compete with it. Instead, it operates alongside insurance as a planning, coordination, and optimization layer—one that remains compatible with employer-sponsored plans, individual coverage, and Medicare pathways. Insurance continues to play its essential role in protecting against high-cost events. FLOW addresses what insurance does not: longitudinal planning, proactive coordination, and alignment between care, cost, and personal health goals.

This distinction is especially important for grey-zone individuals. Their needs span both worlds.

FLOW fills this structural gap by separating health decisions from insurance incentives [/how-flow-pays-for-health-and-longevity-without-insurance], allowing planning, assurance, and insurance to be aligned to real risk rather than blunt categories.

Planning Beats Claims for Ongoing Risk

Insurance is optimized for processing claims after something has happened. Longevity care is optimized for reducing the likelihood that those claims occur in the first place. Planning enables coordination across providers, services, and time, supporting early intervention at lower intensity and lower cost.

For people living in the grey zone, the goal is no longer to “fix” a problem after it becomes severe, but to manage risk intelligently so stability is maintained. This shift—from episodic response to continuous planning—is foundational to better outcomes, lower volatility, and a more humane experience of care.

The Economics of Chronic Care — Without Catastrophe Thinking

Chronic Does Not Automatically Mean Catastrophic

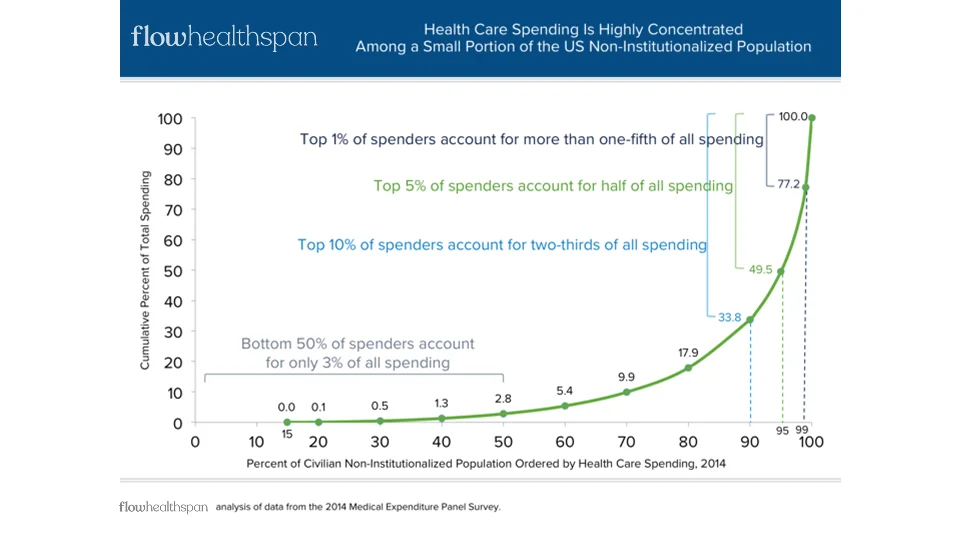

One of the most persistent misconceptions in healthcare finance is that chronic conditions inevitably lead to catastrophic cost. In reality, most grey-zone individuals do not generate extreme, unpredictable claims year after year. Their costs are often higher than average, but they are also more stable, more foreseeable, and highly sensitive to how care is managed over time.

What drives escalation is not chronicity itself, but poor coordination, delayed intervention, and reactive decision-making. Catastrophe is often the result of mismanagement, not inevitability.

Customizing Spending, Assurance, and Insurance to Real Risk

Grey-zone individuals sit between two extremes, yet most systems force them to choose one. FLOW separates spending, assurance, and insurance into distinct but coordinated layers—aligning financial tools with actual risk rather than blunt categories.

Planned, recurring services can be funded directly and predictably. Mid-range variability can be addressed through structured assurance. Truly catastrophic risk remains insured.

Cash Rates, Direct Care, and the Real Cost of Stability

Many services central to maintaining stability are not inherently expensive. They become expensive when routed through insurance. Direct access, cash rates, and coordinated preventive care often cost less while improving continuity.

Grey-zone care is utilization-heavy but intensity-light. Frequent touchpoints matter more than rare emergencies.

Better Outcomes Are Also Better Economics

Proactive care is not just clinically preferable—it is economically rational. Earlier, lower-intensity intervention reduces volatility and long-term cost without denying care or eliminating insurance.

Understanding the Real Risk of High-Cost Events

A more honest discussion requires shifting from fear to probability. Five-figure annual costs—while meaningful—are not catastrophic in insurance terms, and they are often overstated when inferred from claims data alone.

When care is coordinated and accessed directly, the underlying cost of maintaining stability is frequently much lower than insurance-based assumptions suggest.

When High-Cost Insurance Makes Sense — and When It Doesn’t

There are circumstances where robust catastrophic coverage is appropriate and necessary. The critical task is determining when high-cost insurance is justified and when it is excessive.

By separating ongoing care from catastrophic protection, FLOW allows individuals and employers to avoid paying for risk they are unlikely to realize while remaining protected against events they cannot absorb. This distinction is especially important for grey-zone populations, where misaligned coverage—driven by structural limitations rather than true need—often increases cost without improving outcomes.

What the Grey Zone Means for Employers and the System

Why Grey-Zone Individuals Drive Disproportionate Employer Cost

Grey-zone employees are rarely the most visibly expensive in a given year, but they create steady cost and volatility over time. Their needs are persistent, not episodic, making them difficult to manage with traditional levers. What’s missing is a structured layer between routine benefits and catastrophic coverage—one focused on planning, continuity, and coordination. This is why execution in the grey zone requires coordinated guidance [/why-longevity-care-requires-teams], not isolated expertise.

Why Traditional Employer Health Models Fall Short

Employer strategies tend to focus on wellness or high-cost case management. Grey-zone individuals fall between these models, leading to blunt interventions that suppress spend without improving stability.

Structured Support Without Over-Insurance

Over-insuring manageable risk is inefficient; under-supporting it is destabilizing. What’s missing is a structured layer between routine benefits and catastrophic coverage—one focused on planning and continuity.

FLOW as the Missing Coordination Layer

FLOW provides proactive planning, longitudinal coordination, and financial alignment without requiring employers to redesign their benefits. This approach scales—reducing volatility across the entire population.

Prepared, Not Cheap — The Point of Getting This Right

This Isn’t About Minimizing Spend

The goal is not cheaper care. It is appropriate, aligned, and sustainable care—clinically and fiscally effective over time.

Preparedness reduces volatility and preserves health by preventing escalation, not by denying care.

Who the Grey Zone Is Actually Built For

Grey-zone populations are signals, not exceptions. They reveal where traditional models fail and where flexible systems succeed.

FLOW reframes how care, cost, and risk align across a lifetime. As populations age, the grey zone becomes the norm—and systems built to support it become essential.