The Upside Down Economics of Healthcare Costs

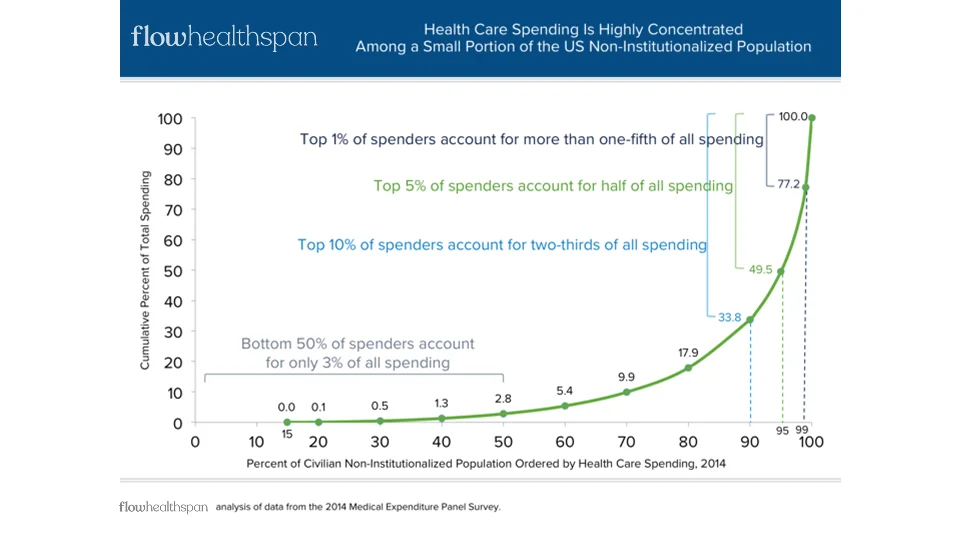

Healthcare finance is structurally inverted. A small fraction of people account for the majority of total healthcare spending, while the overwhelming majority contribute relatively little.

- 1% of the population drives approximately 20% of annual healthcare spending

- 5% drives roughly 50% of annual healthcare spending

This distribution is not subtle, and it is not controversial. It has been one of the most consistent findings in healthcare economics for decades. Yet nearly every part of the healthcare system is built as if this reality were incidental rather than defining. The system simply accepts it.

In a typical year, a small percentage of individuals—often those experiencing acute illness, progressive chronic disease, or end-of-life care—drive a disproportionate share of total costs. Meanwhile, the vast majority of people remain relatively healthy, interacting with the system intermittently and predictably. If health were preserved earlier, decline delayed, and fewer people entered the high-cost tail of the curve, total system costs would fall dramatically.

- The healthiest 50% of the population accounts for only ~3% of total annual healthcare expenditures

But that is not what happens.

Instead, the healthcare financial system is optimized around this failure curve. Revenue, reimbursement, and institutional growth are concentrated where costs are highest—after health has already broken down. The system does not merely respond to illness and disease; it is financially dependent on them. As more people move into the expensive tail of the distribution, more money flows through hospitals, insurers, and intermediaries. Rising costs are not treated as a signal of failure, but as justification for higher premiums, expanded billing, and increased complexity.

This inversion matters because it defines what the system is capable of doing. A system designed around late-stage disease cannot meaningfully prioritize prevention, even when prevention is scientifically sound and economically efficient. The incentives are misaligned from the start: the system is paid to manage disease, not to avoid it. Effort applied upstream—before care becomes expensive—is not simply overlooked; it is actively disincentivized because it reduces downstream revenue. In this structure, insurers, hospitals, and providers lose financial leverage when people remain healthy.

The result is a healthcare economy that grows larger as health outcomes worsen. Costs rise, complexity increases, and responsibility becomes diffuse, while the underlying distribution—the small group driving most of the spend—remains largely untouched until it is too late. This is not a failure of medicine, data, or good intentions. It is the predictable outcome of a system built upside down from the start.

It cannot be fixed.

It must be replaced.

Health Insurance Is Built for Disease Management, Not Prevention

Health insurance plays a critical role in modern society, but it is often misunderstood. Insurance is not designed to produce health; it is designed to manage financial risk once disease occurs. That distinction matters, because it explains why prevention remains perpetually underfunded despite overwhelming evidence of its value.

At its core, insurance exists to pool risk across large populations and pay for unpredictable, high-cost events when they occur—and critically, when they may not occur. This model works well for acute injuries, rare diseases, and catastrophic medical events—situations where costs are large, uncertain, and unevenly distributed. Chronic disease, metabolic decline, and age-related deterioration do not fit this profile. These conditions are progressive, largely predictable, and strongly influenced by behavior, environment, and early intervention.

Yet modern health insurance is overwhelmingly focused on these long-term conditions—not to prevent them, but to manage them once they appear and persist.

This creates a fundamental conflict: meaningfully reducing disease reduces the financial activity the system is built to manage. Premium structures, reimbursement models, utilization forecasts, and risk adjustments are all constructed around the expectation that disease will occur, continue, and intensify over time. When disease is delayed, avoided, or substantially reduced, the financial machinery of insurance has little to optimize around. The system becomes unwittingly—but unavoidably—trapped in a business model that sustains itself by managing disease.

As a result, prevention is treated as optional, secondary, or external to the system. Even when preventive measures are covered, they are typically narrow, episodic, and disconnected from long-term accountability. Screening replaces intervention. Guidelines replace personalization. Health becomes something monitored occasionally rather than actively preserved.

Once an individual crosses into the disease-management phase, a highly complex and fragmented system activates. Claims are paid, specialists are involved, medications are prescribed, and utilization increases—often around the individual rather than under their control. From a financial perspective, this is the system functioning as designed. From a health perspective, it is already behind.

The more disease that must be managed, the larger the system becomes. Administrative layers expand. Billing codes multiply. Complexity increases to manage increasingly nuanced cases, reinforcing rising premiums and expanding reimbursement. Disease is not the explicit goal—but it becomes the condition that sustains the system.

This is why prevention cannot meaningfully scale within traditional health insurance. A system optimized to manage disease cannot simultaneously optimize to eliminate it. The incentives run in opposite directions. Gains made upstream through prevention are diluted downstream, where financial gravity is strongest.

Understanding this distinction is critical. The failure of prevention is not due to lack of knowledge, motivation, or technology. It is the predictable outcome of asking a disease-management system to do something fundamentally opposed to its design.

That limitation sets the stage for why a different model is required.

Why Inefficiency Drives Higher Healthcare Costs

In most industries, inefficiency is punished. Waste increases costs, reduces competitiveness, and eventually forces correction. Healthcare operates under a different set of rules. In healthcare finance, inefficiency is not only tolerated—it is reinforced.

As costs rise, the system does not contract or simplify. It expands. Higher spending justifies higher premiums, larger reimbursements, more administrative infrastructure, and increasingly complex billing and compliance frameworks. Complexity becomes evidence of necessity. Waste becomes indistinguishable from care.

This dynamic is not accidental. It is embedded in how healthcare is financed, regulated, and reimbursed. When costs increase, insurers adjust premiums. Providers negotiate higher rates. Intermediaries add services to manage growing complexity. Each layer exists to manage the consequences of inefficiency rather than eliminate its cause.

The result is a system where rising costs are treated as validation rather than failure.

Administrative burden is a clear example. A substantial and growing share of healthcare spending is devoted not to care delivery, but to billing, coding, utilization management, prior authorization, and compliance. These functions exist to navigate an increasingly opaque system, yet each new layer justifies its own existence by pointing to the complexity beneath it.

Importantly, this complexity is not experienced as choice or control by individuals. It is experienced as fragmentation. Care is spread across providers, specialties, networks, and billing entities, none of which are accountable for the whole. Financial responsibility becomes opaque, outcomes become diffuse, and individuals are left navigating decisions they did not design and cannot meaningfully understand, let alone influence or control.

As inefficiency grows, so does the distance between cause and effect. Outside of the individual receiving care, no participant in the system benefits from simplifying it. Simplification would reduce billable activity, compress margins, or eliminate entire categories of work. In this environment, cost containment is framed as risk rather than progress.

This creates a compounding effect. Disease increases utilization. Utilization increases complexity. Complexity increases cost. Rising costs then justify further complexity. Each cycle reinforces the next, making the system larger, more expensive, and harder to change—while delivering diminishing returns in health outcomes.

Critically, this spiral does not require bad actors. It functions through rational decisions made within a broken incentive structure. Every participant responds logically to the rules in front of them, even as the collective outcome becomes increasingly irrational and burdened by administration.

This is why healthcare costs continue to rise faster than inflation, wages, and economic growth, despite decades of reform efforts. The system is not failing to control costs; it is succeeding at expanding around them.

As long as inefficiency is a source of revenue rather than a signal to simplify, the system will continue to grow more expensive, more complex, and less responsive to individual needs.

A system that profits from inefficiency cannot regulate itself into efficiency.

That structural reality makes categorical replacement—not reform—the only viable path forward.

How FLOW Delivers Control Over Health, Prevention, and Funding

The failures of healthcare finance are not accidental, and they are not correctable through incremental reform. They are the result of a system designed around disease management, inefficiency, and late-stage intervention. Fixing any single component in isolation—insurance design, reimbursement rates, care delivery, or data—cannot resolve a problem that is structural at its core.

FLOW begins from a different premise.

Rather than attempting to improve a system optimized for health failure and inefficiency, FLOW replaces it with one designed around control—control over outcomes, prevention, and what gets funded. Finance is not treated as a downstream administrative function, but as the primary coordination mechanism that determines behavior across the system.

In the current model, individuals are largely passive participants. Decisions about care, timing, funding, and prioritization are made on their behalf, fragmented across insurers, providers, and intermediaries. Prevention, when it exists at all, is disconnected from accountability and rarely personalized. Health outcomes emerge indirectly, if at all.

Under FLOW, individuals regain agency over their health trajectory by directly controlling the financial decisions that shape it. Funding is aligned upstream, before disease progression, not downstream after costs have already compounded. Preventive actions are treated as first-class investments—explicitly planned, funded, and measured over time.

When individuals control what gets funded, prevention becomes actionable rather than aspirational. Decisions about diagnostics, lifestyle interventions, training, nutrition, recovery, mental health, and longitudinal monitoring are no longer filtered through a disease-management lens. They are evaluated based on their ability to preserve health, delay decline, and reduce the probability of entering the high-cost tail of the system.

Importantly, FLOW does not rely on behavior change alone. It changes the incentives that surround behavior. By aligning financial control with long-term health outcomes, FLOW creates a system where staying well is economically reinforced rather than financially invisible.

As unnecessary healthcare spending is avoided—through delayed disease onset, reduced utilization, and fewer catastrophic escalations—financial capacity is preserved. That capacity does not disappear into rising premiums or administrative overhead. It remains available to be intentionally directed toward real health improvements and optimized longevity.

In other words, FLOW does not require individuals to spend more to achieve better outcomes. It changes where and when money is deployed, allowing healthspan investments to be made directly with resources that would otherwise be lost to inefficiency and late-stage disease management.

This is not a wellness overlay. It is not a coaching platform, an insurance alternative, or a care-navigation tool. FLOW is a financial operating platform for health—one that treats prevention, optimization, and longevity as central objectives rather than side effects.

By delivering complete control over health outcomes, preventive action, and funding decisions, FLOW makes possible what the current system cannot: a durable alignment between individual incentives, long-term health, and material cost reduction.

That alignment is why FLOW does not attempt to fix healthcare finance.

It replaces it.

How FLOW Expands Financial Capacity for Health and Longevity

The most counterintuitive outcome of fixing healthcare finance is not higher spending on health—but more room to invest in it.

In the current system, the majority of healthcare dollars are consumed late, reactively, and inefficiently. Costs compound after disease has progressed, options have narrowed, and interventions are increasingly expensive. Individuals rarely see this as a single decision; they experience it as a slow loss of flexibility. By the time care becomes intensive, the required financial capacity has far exceeded what is manageable.

FLOW changes this dynamic by intervening earlier—before costs escalate and before financial decisions are locked in.

When individuals gain control over what gets funded and when, unnecessary healthcare spend is avoided rather than managed. Delayed disease onset, reduced utilization, and fewer catastrophic escalations are direct financial consequences of earlier, intentional action. Each avoided downstream event preserves capacity that would otherwise be consumed by late-stage care and administrative overhead.

FLOW does not create health investment capital by adding new costs or requiring higher spend. It frees capacity that already exists but is currently lost to inefficiency, fragmentation, and delayed intervention in support of a small minority. By preventing avoidable expenses, FLOW makes it possible to redirect resources toward long-term longevity optimization and health management without increasing overall cost—and often while reducing it.

This shift fundamentally changes the economics of health and longevity. Investments in diagnostics, prevention, training, nutrition, recovery, mental resilience, and longitudinal monitoring become sustainable because they are funded with dollars that would otherwise be spent reacting to disease. Healthspan extension stops being an additional expense and becomes a rational reallocation.

Importantly, this is not about extracting savings or promising returns. It is about preserving optionality. Individuals retain the ability to decide how financial capacity is deployed over time, rather than having those decisions dictated by crisis and coverage rules.

As health is preserved, financial flexibility increases. As financial flexibility increases, earlier and more effective interventions become possible. This creates a reinforcing loop—one where better health supports better financial outcomes, and better financial outcomes support better health.

That loop cannot exist in the current healthcare system, where money is deployed only after disease appears.

FLOW makes it possible by expanding health and longevity financial capacity—quietly, structurally, and without requiring more spending to get there.

Why FLOW—and Why the Current Healthcare System Must Be Replaced

The conditions that make FLOW necessary have been building for decades. The healthcare cost curve has long been real—and it has become structurally unsustainable, crippling employers while failing to deliver adequate health outcomes. Disease-driven spending, administrative expansion, and late-stage intervention have reached a scale where inefficiency cannot be absorbed. At the same time, the science of prevention, longevity, and early intervention has matured, and individuals now generate more data about their health than ever before. What has been missing is not awareness, knowledge, or technology, but a financial platform capable of integrating control, prevention, and funding at scale.

FLOW exists because the gap between healthcare finance and healthspan must be closed. The existing healthcare model cannot self-correct, and incremental reform cannot realign incentives that are structurally inverted. Control, prevention, and funding must be unified within a single system, or they will remain fragmented and ineffective. FLOW brings those elements together—replacing a model that reacts late with one that engages early through individual agency, and aligning healthspan and longevity optimization with rational financial design.